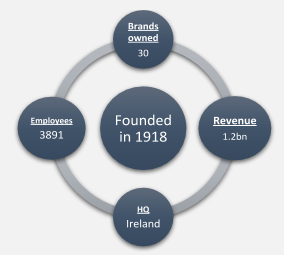

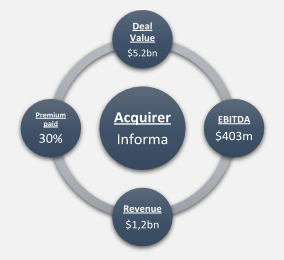

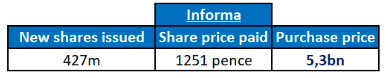

Informa plc. is Britain’s multinational business intelligence and exhibitions group.Informa owns numerous brands including CRC Press, Fan Expo, Institute for International Research, Lloyd’s List (London Press Lloyd), Penton, Routledge, Taylor & Francis.

{kind=link}